Posts made by author 'Ian Brooks-Miller'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2026 | 33 Posts

- 2025 | 48 Posts

- 2024 | 48 Posts

- 2023 | 48 Posts

- 2022 | 46 Posts

- 2021 | 46 Posts

- 2020 | 46 Posts

- 2019 | 31 Posts

- 2018 | 1 Posts

- 2017 | 9 Posts

17

June 2026 Bradenton & Manatee County Real Estate Market Update

Local market data as of July 17, 2026 · Source: REALTOR® Association of Sarasota and Manatee (RASM)

The June 2026 numbers are in, and the Bradenton and Manatee County market is moving in two directions at once. Single-family home prices are rising while inventory keeps shrinking — a seller's market. Condos and townhomes are doing the opposite: prices are flat to down, and buyers have more room to negotiate. Which market you're in changes your whole strategy.

The short answer: In Manatee County, single-family homes are firmly a seller's market (4.1 months of supply, prices up 11.4%). Condos are closer to a buyer's market (more supply, prices down slightly). Same county, opposite conditions.

Is Bradenton a seller's market right now?

For single-family homes, yes. Manatee County single-family closed sales jumped 26.2% year-over-year in June — the largest gain of any local segment — while active inventory fell 15.3%. Months supply dropped to 4.1, well below the roughly six months considered balanced. Well-priced homes went under contract in a median of 45 days. When supply is that tight and demand is climbing, sellers who price correctly have the leverage.

Manatee County single-family homes — June 2026

| Metric | June 2026 | Year-over-Year |

| Closed sales | 890 | +26.2% |

| Median sale price | $490,000 | +11.4% |

| Median time to contract | 45 days | −19.6% |

| Months supply | 4.1 | −21.2% |

| Median % of original list received | 95.8% | +1.6% |

Why are Bradenton condo prices falling?

The condo and townhome market tells a different story. Manatee County condo sales rose 11.2% in June, but the median price eased 0.9% to $310,000 and the median time to contract stretched to 84 days — up from 68 a year ago. Buyers in this segment have more choices and more negotiating room. Rising insurance costs and association fees have cooled demand in parts of the condo market statewide, so it pays to look closely at a building's finances before you buy.

Manatee County condos & townhomes — June 2026

| Metric | June 2026 | Year-over-Year |

| Closed sales | 259 | +11.2% |

| Median sale price | $310,000 | −0.9% |

| Median time to contract | 84 days | +23.5% |

| Months supply | 5.7 | −23.0% |

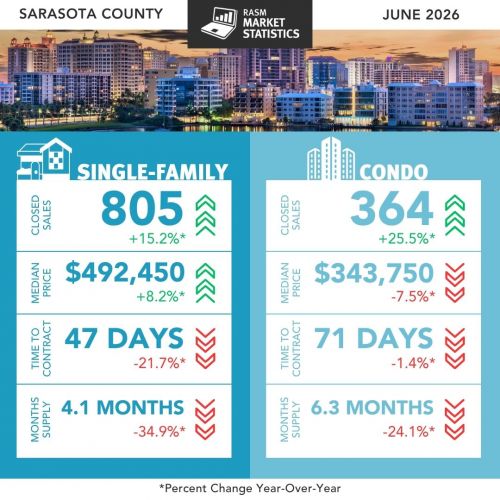

What about Sarasota County?

The same split shows up next door. Sarasota County single-family sales rose 15.2% with the median price up 8.2% to $492,450, and single-family inventory fell 27.4% — the sharpest supply drop in the region. Sarasota condos followed the softer pattern, with the median down 7.5% to $343,750. Across both counties, inventory tightened in every segment while sales accelerated heading into summer.

What does this mean for you?

If you're selling a single-family home: conditions favor you, but the data also shows buyers are rewarding homes that are priced right — sellers received a median of 95.8% of their original list price. Overpricing still sits; correct pricing sells fast.

If you're buying a condo or townhome: you have more leverage than single-family buyers right now. More supply and longer market times mean room to negotiate — just budget carefully for insurance and association costs.

If you're relocating or using a VA loan: the single-family squeeze makes preparation and fast, informed offers matter more than ever. Knowing which micro-market fits your situation is half the battle.

Want to know what your specific home or neighborhood is doing?

These are county-wide numbers — your street can tell a different story. I pull live comps any time.

What's My Home Worth? Start Your Home SearchFrequently asked questions

Is now a good time to sell a home in Bradenton?

For single-family homeowners, June 2026 data shows strong conditions: low inventory (4.1 months), rising prices (+11.4% year-over-year), and homes selling in a median of 45 days when priced correctly.

Are condo prices going down in Manatee County?

The median condo price dipped 0.9% year-over-year to $310,000 in June 2026, and homes are taking longer to sell (84 days), giving buyers more negotiating room than the single-family market.

What is the median home price in Manatee County?

In June 2026, the median single-family sale price was $490,000 and the median condo/townhome price was $310,000.

Where does this market data come from?

The figures are from the REALTOR® Association of Sarasota and Manatee (RASM), compiled by Florida Realtors® from Stellar MLS, released July 17, 2026. Full reports are at myrasm.com/statistics.

Ian Brooks-Miller is a REALTOR® with Wagner Realty, an Operation Iraqi Freedom veteran, and a Military Relocation Professional (MRP). He works with buyers and sellers throughout Bradenton, Lakewood Ranch, Anna Maria Island, and Manatee and Sarasota Counties. Call or text 941-807-4609.

Ian Brooks-Miller, REALTOR®, Wagner Realty. Ian operates as a Transaction Broker under Florida law. Market data is from the REALTOR® Association of Sarasota and Manatee (RASM) / Florida Realtors®, compiled from Stellar MLS, and is believed accurate but not guaranteed. This is general market information, not a prediction or guarantee of any outcome for a specific property. Equal Housing Opportunity.

15

Florida Hometown Heroes Is Funded Again — Up to $35,000 for Bradenton Buyers, and Veterans Get a Break Most People Miss

Florida's Hometown Heroes down payment assistance program relaunched on Monday, July 13, 2026 with $50 million in new funding. Eligible buyers can receive up to $35,000 toward a down payment and closing costs. It's first come, first served — and the last round of $50 million was fully committed in about six months. If you've been waiting for this, the window is open now.

The part almost nobody mentions

If you're a veteran, Florida waives the first-time-buyer requirement — you can have owned a home before and still qualify. Veterans are also generally exempt from the eligible-employer requirement that applies to everyone else. That's a meaningful advantage, and in my experience most veterans have no idea it exists. Confirm your specific situation with an approved lender, but don't rule yourself out because you've owned a home before.

What is the Hometown Heroes program?

Run by the Florida Housing Finance Corporation, Hometown Heroes pairs a 30-year fixed first mortgage with down payment and closing cost assistance for Florida's frontline workforce. Since it launched, it has helped nearly 25,000 Floridians buy homes — including more than 5,200 veterans and military members.

| Hometown Heroes 2026 — the essentials | |

| Funding | $50 million, reopened July 13, 2026 — first come, first served |

| How much | 5% of your first mortgage amount — minimum $10,000, maximum $35,000 |

| What form | A 0% interest second mortgage — not a grant. No monthly payments, but it's repaid when you sell, refinance, transfer the deed, pay off the first mortgage, or move out |

| Who qualifies | Full-time employees of an eligible Florida employer with a physical location — healthcare, K-12 schools, first responders, law enforcement, childcare, courts, and more. Eligibility is based on your employer and work location, not your job title. Veterans and military have their own path |

| Credit | Generally a 640 minimum FICO |

| Loan types | FHA, VA, USDA, and conventional options |

| Property | Primary residence only — single-family, condo, or townhome. Occupy within 60 days of closing |

| Also included | The 1% origination fee is waived, and there are doc stamp and intangible tax exemptions at closing |

You may qualify even if you don't think you do

This is the single biggest misunderstanding about the program, and it costs people money every cycle. Eligibility comes down to who employs you and where you work — not what your job title is.

A cafeteria worker at a K-12 school qualifies. A custodian at a hospital qualifies. You do not have to be a teacher or a nurse. What matters is that you work full-time for an eligible Florida employer at a physical, brick-and-mortar location you report to. (Fully remote employees generally do not qualify, since there's no Florida work location.)

So before you assume you're out, ask. I've watched people talk themselves out of $35,000 because they didn't have the "right" title.

Veterans: read this part twice

I'm a combat veteran and a Military Relocation Professional, and this is the piece I most want to get in front of people who served.

Two of the program's biggest hurdles are generally lifted for veterans:

The first-time-buyer requirement is waived. Most applicants can't have owned a home in the past three years. Veterans generally can — and still qualify.

The eligible-employer requirement is generally lifted. You don't have to be working for a qualifying Florida employer the way other applicants do.

Pair that with a VA loan — no down payment requirement, no monthly mortgage insurance — and Hometown Heroes assistance can go toward closing costs, prepaids, or reducing your principal. That's a real stack of benefits, and very few people are putting these two together.

A note on documentation: active-duty members typically need a current Leave and Earnings Statement, and veterans need discharge under conditions other than dishonorable. Your lender will walk you through it. More on the VA side here: VA Loans in Bradenton → · Veteran Resources →

The honest fine print

I'd rather you go in clear-eyed than excited and surprised later. Things worth knowing:

- It's a loan, not free money. Zero interest and no monthly payments, but the full amount comes due when you sell, refinance, transfer the deed, pay off the first mortgage, or stop living there. Budget for that day.

- Income and purchase price limits apply, and they vary by county. Manatee County has its own figures — ask a lender for the current numbers before you fall in love with a house.

- There are two versions of the program. One counts only the income of borrowers on the loan; the other counts everyone in the household 18 and older. Which one you use changes what you qualify for. This is a lender conversation.

- You only get one shot. Participation in Florida Housing's homebuyer loan programs is one-time, and Hometown Heroes assistance can't be stacked with another Florida Housing DPA program.

- A homebuyer education certificate is required. A few hours online. Knock it out early — don't let it hold up your file.

- You can't reserve the funds yourself. Your lender reserves them in Florida Housing's system, and only once you have an executed contract and a complete file. Which is exactly why being pre-approved now matters.

- There is no fee to apply. Florida Housing says this plainly, and so will I: anyone charging you an upfront fee for "access" to Hometown Heroes is running a scam. Walk away.

What to do this week if you want to use it

The buyers who get this money are not the ones who start looking after they hear the program is open. They're the ones whose files were already sitting ready. Working backward from a reservation:

| Your move order | |

| 1. Right now | Talk to a lender approved for Florida Housing programs. Confirm eligibility, income limits for Manatee County, and which version of the program fits you. |

| 2. This week | Get fully pre-approved. Not pre-qualified — pre-approved, with documents in. |

| 3. This week | Complete your homebuyer education course. Certificate's good for two years. |

| 4. Then | Find the home — within the county's purchase price and loan limits. Your lender reserves the funds once you're under contract. |

If you don't have a lender, I'm happy to point you toward people who actually know these programs. That referral costs you nothing and it's the difference between reserving funds and reading about them later.

|

Not sure if you qualify? Just ask. Tell me where you work and what you're hoping to buy, and I'll give you a straight answer about whether Hometown Heroes is worth pursuing — and connect you with a lender who can actually reserve the funds. No pressure, no pitch. If it's not a fit, I'll tell you that too. Ask Me About Hometown Heroes First-Time Buyer Guide |

Keep reading

Moving to Bradenton · First-Time Home Buyers · VA Loans in Bradenton · Veteran Resources · Home Buyers Guide

Hometown Heroes: frequently asked questions

Is Florida Hometown Heroes funded right now?

Yes. The program relaunched on July 13, 2026 with $50 million in funding. Reservations are first come, first served through participating lenders, and the program pauses when the money is committed. The previous $50 million round was fully committed in roughly six months.

How much money can I get from Hometown Heroes?

Up to 5% of your first mortgage amount, with a minimum of $10,000 and a maximum of $35,000, toward your down payment and closing costs.

Is Hometown Heroes a grant?

No. It's a 0% interest second mortgage with no monthly payments. You repay the full amount when you sell, refinance, transfer the deed, pay off your first mortgage, or move out of the home. There is no prepayment penalty.

Do veterans have to be first-time buyers to use Hometown Heroes?

Generally no. Florida waives the first-time-buyer requirement for veterans, and veterans are also typically exempt from the eligible-employer requirement. If you served and previously owned a home, you may still qualify — confirm your situation with an approved lender.

What jobs qualify for Hometown Heroes?

Eligibility is based on your employer and work location, not your job title. Full-time employees of eligible Florida employers with a physical location — hospitals, K-12 schools, fire departments, law enforcement, childcare centers, courts and more — can qualify. That includes support staff, not just licensed professionals. Fully remote workers generally do not qualify.

Can I use Hometown Heroes with a VA or FHA loan?

Yes. Hometown Heroes assistance can pair with FHA, VA, USDA, and conventional first mortgages. A lender approved for Florida Housing programs can tell you which combination is strongest for your situation.

How do I reserve Hometown Heroes funds?

You can't reserve them yourself. Your lender reserves the funds in Florida Housing's system, and only after you have an executed sales contract and a complete file. That's why getting pre-approved before you shop matters so much when funding is limited.

|

Ian Brooks-Miller, REALTOR® Wagner Realty · Military Relocation Professional · Combat Veteran I'm a Bradenton REALTOR® who works with buyers and sellers across Manatee and Sarasota County, with a focus on veterans, military families, and first-time buyers. I help people make informed decisions — and I'll always give you the honest read, not a sales pitch. Call or text: (941) 807-4609 · IanFLRealtor@gmail.com · iansellsflorida.com |

Ian Brooks-Miller is a licensed real estate professional with Wagner Realty and operates as a Transaction Broker under Florida law. I am not a mortgage lender and this is not lending, tax, or legal advice. Program terms, funding availability, income limits, purchase price limits, and eligibility requirements are set by the Florida Housing Finance Corporation, are subject to change, and must be verified with an approved lender and at floridahousing.org. Information here is believed accurate as of July 14, 2026 but is not guaranteed. Nothing on this page is a guarantee of loan approval, program eligibility, funding availability, or any other outcome. Equal Housing Opportunity.

7

New VA Loan Appraisal Rules for 2026: What Veteran Buyers in Bradenton Should Know

If you're a veteran shopping for a home right now, there's good news out of the VA. As of May 1, 2026, the VA updated the property rules its appraisers follow — and the changes are squarely in your favor. The goal is to cut outdated red tape that used to trip up perfectly good deals, so veteran buyers can compete and close faster in a tight market.

As a veteran and a Military Relocation Professional here in Bradenton, I want to break this down in plain English — what actually changed, what it means for you at the closing table, and what to watch for here in Florida.

First, what a VA appraisal actually does

Every VA purchase loan requires a VA appraisal — it isn't optional, and you can't waive it....

29

Celebrating America's 250th: July 4th in Bradenton & on Anna Maria Island

This year's Fourth of July is unlike any in our lifetimes. On July 4, 2026, the United States turns 250 — the semiquincentennial — and our corner of the Gulf Coast is marking it in a big way. As a veteran, this one means a great deal to me, and I wanted to put together a simple local guide so you and your family can be part of it.

From the island's beloved water-fight parade to one of the largest celebrations in Bradenton's history, here's where the Suncoast is coming together to celebrate 250 years.

On Anna Maria Island: the Privateers' Parade

The island's signature Fourth of July tradition is the Anna Maria Island Privateers' Independence Day Parade — a free, famously soggy, all-in-good-fun eve...

4

Hurricane Season Prep for Bradenton Homeowners: Your Gulf Coast Checklist

The Atlantic hurricane season opened June 1 and runs through November 30 — which makes early summer the right time to get ready. Not because a storm is bearing down this week, but because the calmest, smartest decisions get made before one is ever named. If you live in Bradenton, on Anna Maria Island, or anywhere across Manatee and Sarasota County, a little preparation now buys a lot of peace of mind later.

Here's the short version of what matters most. For the full walkthrough — including a printable supply checklist and a one-page quick reference — grab the free Gulf Coast Hurricane Preparedness Guide.

Know your evacuation level first

The greatest threat to life in...

|

|